Cash splash as Boomers hit the jackpot

After decades of saving, older Australians are spending up. But the wave of cash is causing headaches for the inflation-fighting treasurer and RBA. Can the good times last?

Kacy Grainger’s good fortune has been to establish the gallery in a city crawling with cashed-up former senior public servant

Canberra art dealer Kacy Grainger is in no doubt the market for original paintings and sculptures has shifted since the middle of last year.

Interest rates are up. Customer numbers are down. But when she and her husband Richard looked more closely at their sales data, something strange appeared.

“Sales volume dropped off, but our gross revenue was sitting only slightly down,” says Grainger, who opened her gallery in Canberra’s revitalised Dairy Road precinct near the industrial area of Fyshwick just over three years ago.

Works from established and up-and-coming artists priced between $1500 and $3000 are not heading out the door like they used to. But fears that higher-end works would struggle to find buyers – like those for the stunning colour saturated still life oil paintings by Byron Bay-based Gatya Kelly that sell for as much as $15,000 – were misplaced.

“We realised that most of our sales were of larger, more expensive works that were going to self-funded retirees,” Grainger tells AFR Weekend. “It’s the boomers that are spending, and our younger clientele have really dropped off.”

Grainger’s good fortune has been to establish the gallery in a city crawling with cashed-up former senior public servants living off hefty defined Commonwealth superannuation funds.

But the consumer market “bifurcation” – as some economists have dubbed the trends seen by Grainger – are not unique to Canberra.

Baby Boomers around the country are doing very well – according to spending data – while younger generations of mortgaged householders and renters find themselves in a death squeeze between high-interest rates and galloping inflation.

The diverging experience of young versus old shows no signs of slowing down, either, especially for those living off fixed-interest assets like bonds or term deposits, which are generating a sharp rise in income thanks to elevated yields – an under-appreciated consequence of the global interest rate hiking cycle. And the more central banks hike, the better it gets for asset rich, heavily “financialised” older households.

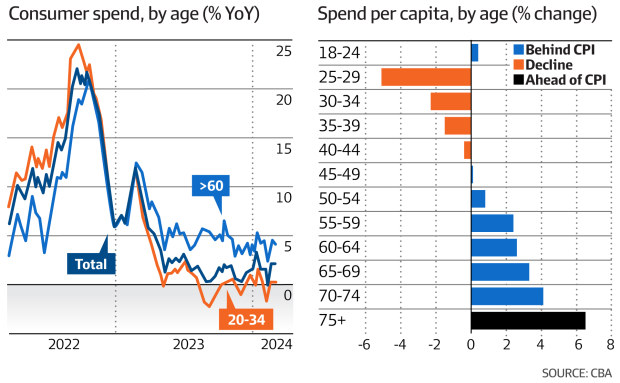

Figures based on Commonwealth Bank of Australia customer data show overall spending per head of population grew at a slower pace than inflation in the first three months of the year.

Only those aged 65 or more recorded spending that outpaced the rate of inflation, an unusual reversal of the normal historical caution displayed by older consumers.

This can be explained by the fact that younger people have suffered the biggest hits to spending power, with mortgages, rents and federal government tax “bracket creep” constraining their ability to put money into other things, says CBA economist Gareth Aird.

“If you generalise, older people don’t have mortgages,” he says. “A lot of people in that age bracket aren’t renting, so they haven’t been hit through rate hikes in a material way, they haven’t been hit through bracket creep. A lot of people on the aged pension have seen the pension indexed to reflect inflation, and all those with deposits are getting a higher return than previously,” he says.

“The story in all of this is that, through the various levers that have been pulled to get inflation down, they’ve landed hardest on those with mortgages and on renters.

“That picture will start to change when the RBA is finally able to ease, but we’re not there, so I wouldn’t expect these trends to shift in the short-run.”

Both here and abroad, that lop-sided consumer picture – increasingly driven by the shift to retirement of the demographic “Boomer” bulge made up of people born between 1946 and 1964 – is complicating the inflation-fighting challenges faced by central banks, and adding to budget policy headaches for Treasurer Jim Chalmers.

At the political level, it could ultimately reignite intergenerational conflict, providing fresh fuel to advocates of greater taxation of wealthy retiree savings to ease the burden on younger taxpayers.

Labor tried to tackle intergenerational inequity in the 2019 election and ended up triggering the wrath of older voters when it promised to introduce changes to franking credits, a key reason Bill Shorten lost to Scott Morrison.

While Chalmers has no political appetite to go there again – notwithstanding last year’s still-to-be legislated promise to double the tax paid on earnings on superannuation balances above $3 million – the issue of how different generations bear economic burdens could erupt anew as the spending differentials get worse.

This month’s shock inflation data showing underlying inflation running hot at 4 per cent a year has hit Labor like a sledgehammer, eroding hopes the Reserve Bank of Australia will deliver the first interest rate cuts of this cycle ahead of the next election.

Jim Chalmers and the government are grappling with cost-of-living pressures. James Brickwood

This month’s budget is being framed around that reality, with Chalmers forced to push back against endless demands for greater spending commitments for fear of worsening the inflation outlook.

Which is why the Boomer spending boom is so problematic.

For decades that cohort has done as they were told and pumped money into their superannuation accounts. But as the generation that has lived through the greatest era of broad-based wealth creation in history shifts off the “accumulation” phase, they will alter the economic dynamics of consumption.

Perversely, the more interest rates rise and the longer they stay high, the better life is likely to be for asset rich Boomers relative to younger Australians.

Unlike the last time in the early 1990s when the Reserve Bank was forced to cool the economy with heavy interest rate hikes, excluding the rising inflation episode of the mid-2000s when the global recession triggered by the global financial crisis ultimately did much of the work, the demographic impact of Boomer spending on monetary policy is more novel.

“It’s something we never thought about at the start of the hiking and a lot of people missed it,” says Nic Guesnon, an economist at UBS. “Everyone focuses on increases in mortgage repayments, but not everyone looks at net interest paid.”

Asset-loaded older Australians are highly liquid. They can draw cash out of super and sell holdings such as exchange-traded funds instantly, and are less tied down by lumpy assets like one or two investment properties. They now have the mandatory income stream flowing from Australia’s $3.5 trillion superannuation pool, and there’s simply so many more of them as a proportion of the overall population compared to 30 years ago.

“There’s a lot of financialisation of older household balance sheets that’s muting the impact of rate hikes, relative to even 10 years ago, and superannuation is one of them,” says Guesnon.

UBS estimates that retirement benefits paid ballooned last year by nearly 7 per cent to a record $149 billion.

For context, that drawdown is more than six times the size of the value of the stage three tax cuts at around 6 per cent of gross domestic product.

And households over 65 years are the only cohort, in general, to have more cash than debt.

“What that means when rates go up is that they get more interest income,” says Guesnon. “Everyone else throughout the income distribution has net debt, so they lose disposable income via higher interest paid.”

Those older households are also far wealthier than ever before. Across the age groups, the ratio of wealth to income is about 10. But for the 65-and-old group, that figure exceeds 20 and rising.

That means the benefit to income from a small increase in asset values or yields is far greater than any tightening of financial conditions, says Guesnon.

Another factor to consider is the fact that the pool of super savings is growing faster than the economy. Even if draw-down rates continue to average 4 per cent a year, an assumption UBS makes, super’s impact on consumption will only escalate, adding upward pressure to inflation.

Drawdowns from super are expected to increase from around 2.4 per cent of GDP in 2022-23 to 5.6 per cent of GDP in 2062-63.

Little wonder retirees are still in a mood to spend big, even as those with mortgages suffer. It’s a significant reversal from just a few years ago when ultra-low interest rates switched the dynamic.

This is not just a problem for the RBA or Chalmers.

Similar trends have emerged in the US, where the “wealth effect” generated by rising bond rates could prevent the Federal Reserve from cutting interest rates any time soon.

Michele Bullock, governor of the Reserve Bank of Australia will announce the next rates call on Tuesday.

In the past, consumers spent between 4¢ and 15¢ of each dollar of increased wealth via housing and the sharemarket. An analysis of Visa payments data in 2023 suggests that figure has tripled from 9¢ in 2017 to 34¢.

Macro commentator James Aitken said this week that the recent inflation bump may force the Reserve Bank to go further than it already has and revisit its view that the current cash rate of 4.35 per cent is doing enough work.

“Let us therefore think, conservatively, that sufficiently restrictive – as opposed to ‘sufficiently hopeful’ or ‘politically opportunistic’ – monetary policy in Australia requires a 5.25 per cent cash rate,” he said.

That would be terrible news for the Albanese Labor government, reeling under the political fallout of rising cost-of-living pressures. It is frantically trying to portray itself as running a fiscal strategy that brings relief to the vulnerable while ensuring any increased spending does not add to inflation.

Ultimately, next week’s budget must be seen to aid the Reserve Bank rather than make matters worse. But the blunt effects of monetary policy mean Chalmers may need to confront the differing intergenerational experiences of the current cycle.

Other measures may be needed to curb that Boomer splurge.

They could include wealth and capital gains taxes, and reform of the GST in exchange for relief from income tax bracket creep, in which workers find themselves pushed by wage gains into higher tax thresholds.

Economists say those changes could help build budget surpluses and allow the RBA to bring down borrowing costs sooner. But all are politically challenging, requiring courage and will.

In the meantime, Boomers look determined to keep spending.

Grainger says older customers prefer more conservative works, leaving the abstracts and conceptual artists’ works favoured by younger buyers hanging on the gallery walls.

“I had a funny conversation with one person the other day who said ‘we’ve downsized, and now we’re in a modern apartment and none of our collection fits and we really want to buy some modern pieces to match’.”

As for the economic outlook, Grainger tries to “shut out all the Chicken Littles saying we’re headed for recession”.

“I’m just hoping we get a rate cut sooner rather than later.”

Subscribe to gift this article

Gift 5 articles to anyone you choose each month when you subscribe.

Subscribe nowAlready a subscriber?

Introducing your Newsfeed

Follow the topics, people and companies that matter to you.

Find out moreRead More

Latest In Federal

Fetching latest articles